For decades, regular Joes were led to believe that the best way to amass points and miles — and travel around the world in first class for cheap — was to be loyal to airlines and hotels. Sure that works, eventually. But it’s the old and hard way. There’s a better strategy and you don’t need to be a road warrior to reap the benefits. Forget frequent flying; embrace frequent spending.

Life is an endless procession of bills—and you get a whole new batch of expenses when you get married, whether it’s the wedding itself, the honeymoon, the ring, the house you want to buy, the kids you want to raise, or the insurance you need to purchase. The more often you can use credit cards for these and other expenses, the more points and miles you’ll save. But there’s a catch: You can only play this game if you’re paying off credit-card bills in full every month (do use autopay). If you don’t, then you will incur interest, which is the bane of the points-and-miles baller.

Below are the rules that will transform you from a schlub who pays with cash or low-yield credit card (cue: shudder) into a shark who effortlessly absorbs points and miles on a regular basis (cue: slow-clap applause).

Rule #1: Pay off your credit card balance in its entirety every month.

Use auto-pay. Don’t miss any payments. If you can only pay the minimum balance of an existing card, try to migrate that debt to a card with 0% balance transfer.

Rule #2: Use credit cards where you’re already spending regularly.

Identify where you spend money and match the categories of “spend” with the cards that reap the most rewards in each of those categories. Couples can earn serious points, or cash back, when paying for everything from big expenses (movers, rings, meals, air travel, weddings) to smaller ones (groceries, lunch, drug store purchases, gym membership, utilities, groceries, beer).

An average card will give you 1x (1 point or mile) per dollar spent. Your goal is to find ways to get 2X, 3X, 5X, and sometimes even 10X for every dollar you spend. Over time, these points add up and you can use them to book travel or for other purposes, including shopping. If you don’t travel often, and just want the points to help pay off the bills, you’ll want a card that offers a good cash-back rate, like the Citi Double Cash cards offers (2% cash back) or the Alliant Cashback Visa Signature (2.33%+).

But note: Redeeming for flights and hotels almost always gets you maximum value. I recently had 46,135 Ultimate Rewards points and Chase’s website made it clear that I could get 50% better value if I booked a flight or hotel—my points were worth $692.03 in travel dollars, but only $461.35 in cash.

Read our credit card guides for explanations of exactly which cards are best for the following scenarios:

- Best credit cards for buying the ring

- Best credit cards for the honeymoon

- Best credit cards for wedding costs

- Best credit cards for married couples

Rule #3: Be sure to “earn” and “burn.”

When you make a purchase that yields points or miles, you are earning. Anyone who uses the Chase Sapphire Reserve card, for example, earns 3X points on dining (restaurants) and travel (hotels, airlines), which means a $150 meal gets them 450 points. You also earn points when you sign up for a new card and get bonus points (look for deals of 50K or more on signup). Some cards may grant extra points if you make a certain number of purchases in a billing cycle, too.

When you redeem points for travel (or for any category of product), you are burning. Let’s say you found a way to use 50,000 points for roundtrip business class seats to Tokyo — knowing it often costs 100,000 points or more. In that case, you are redeeming/burning like a mensch. How exactly do you find deals like that? See the next category, which discusses transferring points and using airline alliances.

You can also redeem (burn) points for things like Uber rides (with certain American Express cards) and for gift cards at shops, rental car agencies, restaurants, and even Airbnb. But note: These are usually considered poor uses of points as you’ll get only a 1x value (sometimes even less!) instead of 2x or more.

Rule #4: Transfer points and use airline alliances to spot deals

Points and miles junkies get most excited when talking about the art of transferring because it can reap astonishing, surprising returns. Basically, the points and miles you collect may go farther if you transfer them to a partner company to pay for a flight or room–getting you access to cheaper and/or exclusive “award” travel around the world… and into almost every major route and city on airlines you may never otherwise use.

Some of the most popular points programs come from Chase (Ultimate Rewards points), American Express (Membership Rewards points), CitiBank (ThankYou points) and Starwood Preferred Guest (SPG). All of them allow cardholders to transfer points to airline and hotel partners.

There are also three airline alliances; each includes one of the big three US airlines plus a slew of international airlines:

Star Alliance

United Airlines

https://www.staralliance.com/en/

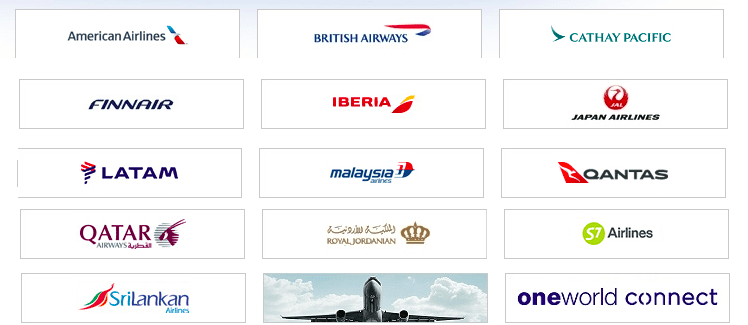

Oneworld

American Airlines

https://www.oneworld.com

Sky Team

Delta Air Lines

https://www.skyteam.com/en

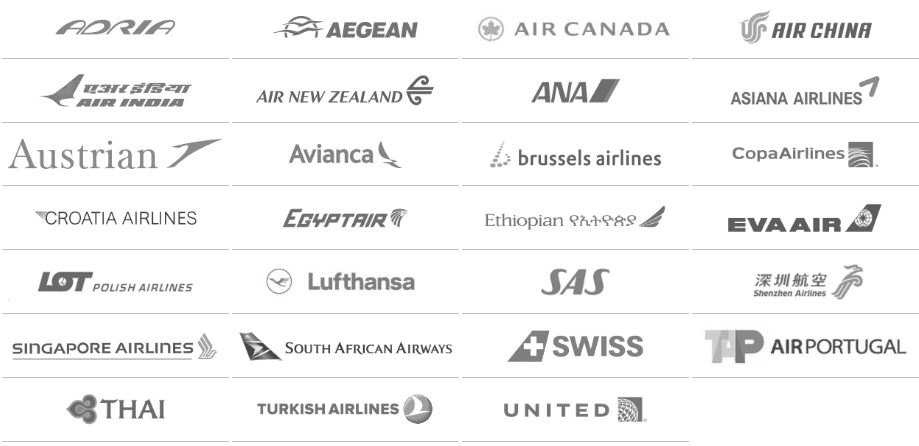

So, for example, you can use United miles to book “award” flights with any of their Star Alliance partners, which includes LOT Polish, Swiss, Thai, and so on.

Rule #5: Develop a strategy with your partner.

You have two chances to own any card when you’re in a relationship. Two credit scores. Two lifestyles. Assuming you don’t maintain debt on credit cards, you and your partner should identify where you spend money (financial apps can help you identify the categories) and then you can then figure out which card gets the maximum amount of points for those categories.

Does she like to have fancy meals once a week? Do you spend a ton on shipping for your small business? There are cards that will maximize the points you get for spending in those categories. Some of the best cards, especially for travel perks, cost the most—around $500 annually—and have steep minimum spend requirements; you may have to spend $3,000 inn three months to get the “bonus points” that lured you to the card. To avoid spending twice that (once for each person), many couples designate “authorized users” instead.

To figure out which credit cards are best for your needs, read these stories:

- Best credit cards for buying the ring

- Best credit cards for the honeymoon

- Best credit cards for wedding costs

- Best credit cards for married couples

Rule #6: Make use of authorized users.

If you’re afraid you can’t spend enough to reach a new credit card minimum in the assigned time frame, then consider making your partner an authorized user. This way, the two of you will earn even more points for one account, and you both get into airport lounges. What’s more, you can help your partner build or repair a credit score. In some cases, you can also transfer your points to and from authorized users; check with your card issuer. While you’re at it, find out if adding someone as an authorized user costs a fee (it can be $95).

Avoid opening joint accounts (some banks don’t even offer this); only one person should control a card. Why? Finances get messy when there’s a breakup in a joint account. With authorized users, one person clearly has final say: the original cardholder.

Rule #7: Sign up for any and all free loyalty programs.

It’s hard not to like free stuff. Lucky for you, just about every loyalty program is free to join. So if you think you may use United, Delta, American or JetBlue, then sign up for their programs on their respective websites. When the time comes to book flights, you can tell the reservationist that yes you do have an account and you will get the points credit. Same goes for hotels: Marriott, Starwood, Hyatt, Hilton, IHG, and so on.

The Points Guy maintains a list of airline, hotel and car rental loyalty programs.

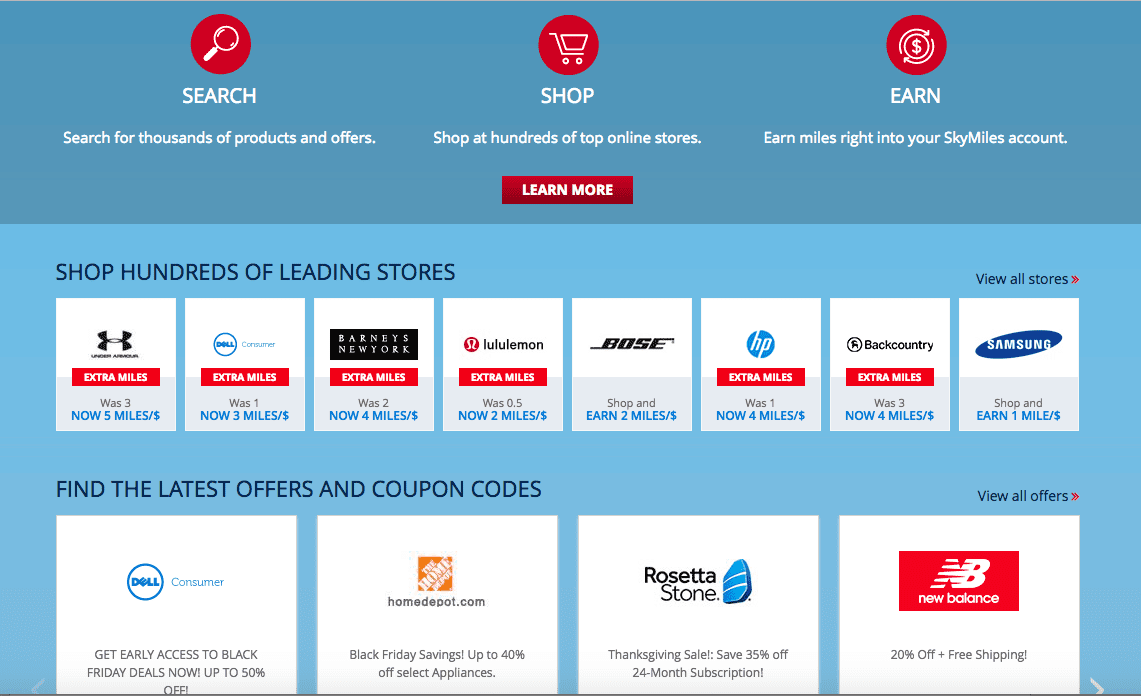

Rule #8: Use shopping portals.

Let’s say you’re planning to buy an item, dish towels, at Bed, Bath & Beyond online. Don’t! Start instead at an online shopping portal, log in, navigate to the BB&B online store there, and note that you will earn extra points for all purchases with no other strings attached. In fact, many of the major chains in the US are available at shopping portals. This includes Home Depot, Samsung, Walmart, Lowe’s Sephora, and Staples. Some stores offer greater discounts than others and there are always seasonal discounts, too.

Popular Shopping Portals

Airlines

- Aeromexico: Mall Premier

- Air Baltic: PINS e-Shop

- Air Canada: Aeroplan eStore

- Air France: Air France Flying Blue Shopping

- Alaska: Mileage Plan Shopping

- Alitalia: MilleMiglia Mall

- All Nippon Airways: ANA Mileage Mall

- American Airlines: AAdvantage eShopping

- British Airways: Gate 365

- Cathay Pacific: Asia Miles iShop

- Delta: Sky Miles Shopping

- e-Miles: e-Miles Market

- Etihad: Etihad Guest Earn Mall

- Finnair Plus: Finnair Plus Shop

- Hawaiian Airlines: HawaiianMiles Online Mall

- Japan Airlines: JAL Shopping Americas

- JetBlue: ShopTrue

- KLM: Shop@KLM

- Miles & More: Miles & More Online Shopping

- Qantas: Qantas Shop

- Singapore Airlines: Krisshop

- South African Airways: Miles for Style

- Southwest: Rapid Rewards Shopping

- United: MileagePlus Shopping

- US Airways:Dividend Miles Shopping Mall

- Virgin America: Elevate Fly Store

- Virgin Atlantic: Shops Away

- Virgin Australia Velocity Frequent Flyer: velocity eStore

Hotels

- Choice Hotels: Choice Privileges Mall

- Hilton: Hilton HHonors Shop-to-Earn Mall

- Marriott Rewards: Shop My Way

Other

- Amtrak: Amtrak Guest Rewards

- Barclays: Barclays RewardsBoost

- Chase: Shop through Chase

- MyPoints: MyPoints Shopping

- Upromise: Upromise

Here’s what the shopping options look like at an airline portal—for Delta Skymiles members in this case.

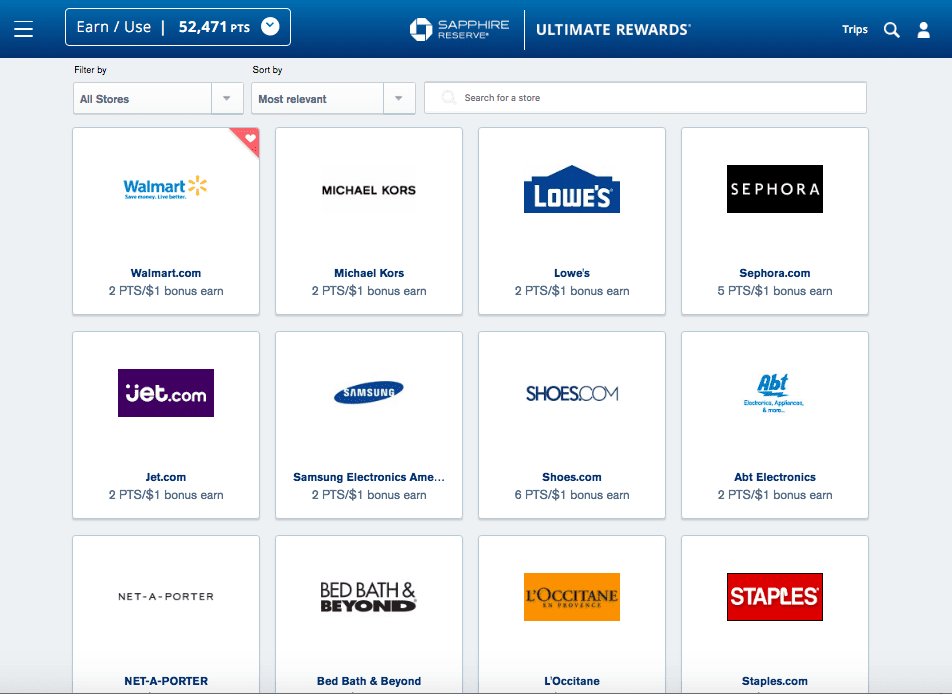

And here’s one at a bank shopping portal—for Chase Ultimate Rewards members.

Rule #9: Keep track of everything.

The only thing worse than not earning points is not using points you’ve actually earned. If you want to squeeze maximum value out of your spending habits and credit cards, you need to develop an easy way to remember which cards you have, what their perks are, how much the minimum spend is, if there is an annual fee, and expiration dates of points/miles.

Some people use spreadsheets. You can download/open free ones developed by super-nerds, but beware; these can be overwhelming. MyPointsBlog offers one such spreadsheet. Or consider customized applications for desktop and mobile including AwardWallet, Points.com’s Loyalty Wallet, and TripIt Pro.

Rule #10: Earn elite status if you travel a lot.

Earlier in this article, we suggested that being loyal to specific brands is the old and hard way of maximizing points and miles. The truth is, it can be a game-changer but only if you travel enough — or spend enough — to make it worth the while.

Let’s say you do travel a lot (at least 25,000 miles or $3,000 annually). If you always fly, say, United and always stay at Hiltons, you will soon find yourself getting perks like seat upgrades, room upgrades, lounge access, priority seating, free checked bags, and more. You become one of their preferred customers. But then it gets complicated because most loyalty programs have three or four tiers: silver, gold, platinum and, perhaps, diamond. And the hierarchies require mastery of proprietary terms. For example, you would need to keep track of, and maintain a minimum number of, miles to keep up with the elite status requirements of the three major airlines…

American Airlines has EQMs — Elite Qualifying Miles

United Airlines has PQMs — Premier Qualifying Miles

Delta Air Lines has MQMs — Medallion Qualification Miles

One way to jump ahead of the pack (or not have to fly or spend so much to get elite status) is to sign up for “co-branded” credit cards that automatically grant you elite status. These are cards that are joint ventures between hotels or airlines and issuers like Chase, American Express, Citi, and Barclays, among others.

Some top co-branded hotel cards:

Some top co-branded airline cards:

Rule #11: Revisit your strategy, cards, and goals.

Life changes. Stuff happens. You need to set a date (maybe January 1, but not necessarily) to stop and take stock of your credit card situation. Do you have the cards you need? Did you use the cards you got? Do you have the same goal or is it time to rethink the strategy? This is an ideal time to talk to your partner so you are coordinated (see rule #5).

Rule #12: Downgrade Cards, Don’t Cancel Them

There will come a moment when you don’t want to keep a certain credit card anymore. Maybe you found a better return on investment with a newer card. Or perhaps you don’t travel as often as you used to. Regardless, the general wisdom for avoiding dings to your credit record is to just pay off any remaining balance and stop using the card rather than canceling it. If it is a card that has an annual fee, then call the company and explain that you want to downgrade to a different (free) card.

For more credit-card advice, read our explanations of exactly which cards are best for the following scenarios:

- Best credit cards for buying the ring

- Best credit cards for the honeymoon

- Best credit cards for wedding costs

- Best credit cards for married couples